Capital efficient price discovery mechanisms will transform markets for nonfungibles and other illiquid assets

Read this on Medium.

Today, most people following nonfungibles observe that it is a very illiquid asset class and feel it is likely to stay that way. What may not be obvious is that, in the context of blockchain’s cryptoeconomic mechanisms, “liquidity” is merely a mechanism design problem being rapidly solved. In this post, I would like to dive into how cryptoeconomics will financialize the NFT space, improve its liquidity profile, and extend this technology to other illiquid assets over time.

The financialization of the NFT asset class

Back in the early stages of the blockchain space it took months, and sometimes years, for a fungible (read: ERC20) token to achieve any significant liquidity. Issuers would compete to get listed on a centralized exchange, pay hefty fees, and jump through regulatory gauntlets. But the market applied smart contracts and cryptoeconomic mechanisms to solve the liquidity problem for fungibles. These days, through the magic of liquidity mining and the ingenuity of automated market makers, the time to liquidity for an average ERC20 token is virtually zero and DEXes are doing upwards of $2B of daily volume while serving $44B of DeFi market cap.

In contrast, the prospects of selling any individual nonfungible in the secondary market are still bleak today, even after a year when NFT GMVs have ticked up dramatically in 2020. In a previous post, I proposed that we design NFTs as “liquid intellectual property.” As the scope of NFTs encompasses more and more digital content, the liquid IP view comes with the implicit assumption that NFTs are, in their own right, a new financial asset class.

As NFTs become increasingly financial, they will require new kinds of exchanges, lending protocols, and derivatives. Thus, I claim that price discovery is the next major problem set in the NFT space. Capital efficient mechanisms for price discovery will enable participants to transact more quickly, improve liquidity through tokenization, allow nonfungibles to be collateral without order books, and create a rich set of derivatives with nonfungibles as underlying. In other words, price discovery will enable the financialization of the NFT asset class.

So how will it be implemented? Once again, as we lay out in this post, new price discovery mechanisms — in particular, appraisal games — will create key innovations that will solve the liquidity problem for NFTs and other illiquid assets.

Understanding current price discovery mechanisms

There are only a few ways that price discovery proceeds in NFTs today. First understanding these mechanisms will help us form a framework for how to think about the price discovery problem.

-

The Sale Mechanism. In the sales approach, used by Rarible and most other NFT marketplaces, valuations are created from an open market public sale. As NFTs exchange hands through sales, the market notes historical prices and provenance of assets. Without an outsized market of participants, this default mechanism doesn’t have too much information about pricing and the market is very illiquid. As we shall see, sales are on the frontier of capital inefficiency: their main drawback is that for every dollar of valuation, someone must actually pay a dollar to create it.

-

The Auction Mechanism. For better or worse, most marketplace sellers and buyers actually prefer auctions for obtaining and pricing NFTs. Async.art uses perpetual auctions as their native gallery, as does SuperRare. Beeple’s storied $3.5 million drop shows that auctions, while career-making, are generally exuberant. It’s worthwhile to note that auctions are well-suited toward art sales, where the intrinsic value of assets tends to be much more subjective and in the eye of the beholder. But from a capital efficiency perspective across general NFT assets, auctions are suboptimal. Most blockchain auction mechanisms in production aren’t Vickrey auctions, which would incentivize participants to bid their true value. Even if they were, they would have even worse capital efficiency than sales: they require capital to be locked up by bidders. (Some platforms have even proposed paying bidders DeFi yield on locked up bid capital to mitigate lockups.) In an auction, for every dollar of valuation, the mechanism might require multiple dollars of worth of bidding.

-

The Fractionalization Mechanism. NFT fractionalization, as seen in the pioneering work of Niftex, is the first innovation toward creating capital efficiency in an NFT price discovery context. Together with other approaches like Ark, Wrapped Punks, WG0, and NFTX.org, fractionalization shards one or more nonfungibles into an ERC20 currency which can gain liquidity on a DEX or centralized exchange. Anyone can buy any amount of the currency in order to help establish the overall valuation, bringing down the cost of valuation for an individual user (but not necessarily in the mechanism as a whole). With fractionalization also come the challenges of stakeholder governance and managing a proliferation of ERC20 assets corresponding to a large universe of nonfungibles.

This discussion of existing approaches motivates the question of whether there exist approaches that dramatically improve capital efficiency for the price discovery problem. We cover some of these approaches in the next section.

Capital efficiency is what makes price discovery disruptive

Based on our discussion so far, a basic framework for evaluating price discovery mechanisms is measuring their capital efficiency. Let us define P(x) as the discovered price of a good x and C(x) as the total cost expenditure from participants required to price it. Then we can broadly define the price discovery efficiency of a mechanism as, informally, E = P/C across a particular set of assets. In this framework, sale mechanisms always have an efficiency of E = 1, auction mechanisms have E ≤ 1, and fractionalization deserves a more nuanced analysis than we should do here, with E ≥ 1. The question is whether we can do much better than fractionalization, and the answer is yes.

-

Price Computation. While auctions are great for subjectively-valued goods, collectibles markets are often pricing on scarcity and well-defined properties. Some assets, like CryptoKitties and virtual real estate, might have pricing that can simply be computed. NFTBank.ai is one of the first startups to put forward accurate machine learning models for predicting the prices of collectibles based on past pricing of similar or adjacent collectibles. Virtual real estate pricing might succumb to models which take into account past sales and revenue generation possible in the neighborhood. In this context, capital efficiency goes way up because we can think of the mechanism as having a fixed cost, c, of deploying the pricing algorithms. Thus the cost will be amortized across price discoveries and efficiency E = P/c will go to infinity over time. Still, the jury may still be out on whether machine learning will work well for exuberant and subjectively-valued goods, like Beeple art.

-

Expert Networks. We don’t necessarily need to build a machine learning model in order to achieve a fixed cost of price discovery. Imagine for each pricing, we pay a fixed amount of money to five experts who give us their educated opinions about a good’s fair market value. Capital efficiency improves as the goods appreciate in value. This approach can use centralized services, or incentivized networks of humans, to create appraisals. One concern with using human experts is scale — will we really have enough experts to process the entire potential volume of goods that the NFT space is likely to produce? As we shall see next, this approach is probably best formalized as on-chain oracle networks, which will naturally incentivize agents to play appraisal games and do so efficiently.

-

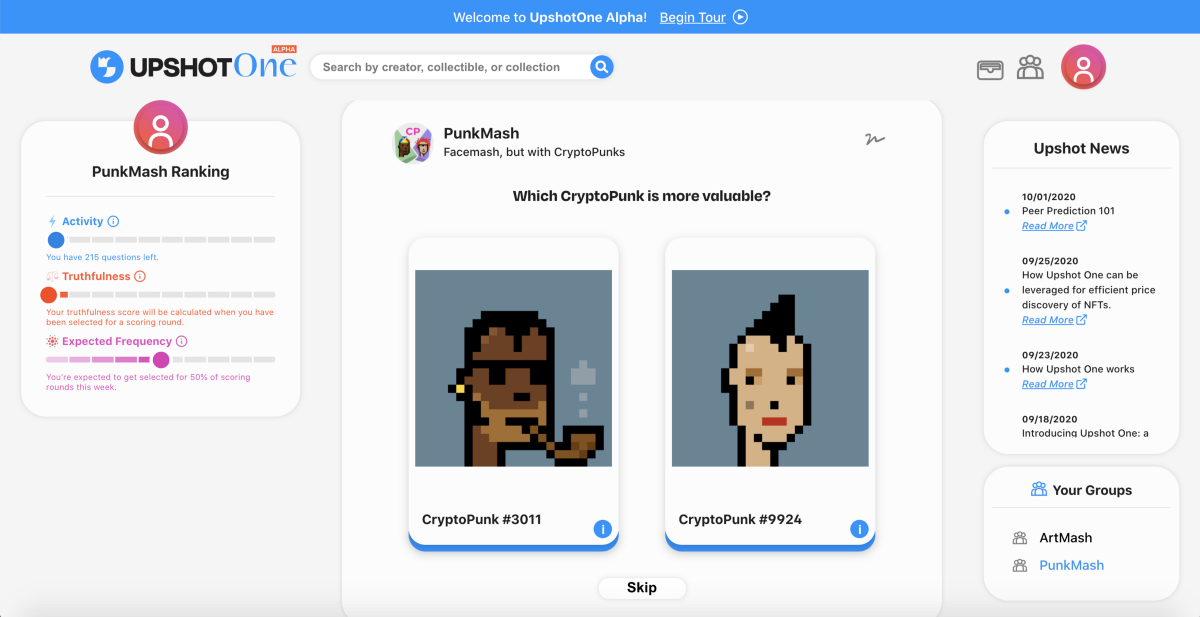

Peer Prediction Oracles. The most exciting recent development in oracles is the implementation of peer prediction as an on-chain mechanism, pioneered by Upshot. Peer prediction is a cooperative game that incentivizes participants to honestly answer queries, without requiring data feeds or other sources of objective ground truth. Upshot proposes to apply peer prediction, coupled with an ordering algorithm, to create capital efficient price discovery for NFTs. It’s hard to do justice to peer prediction in this small space, but the mechanism by nature is agnostic between objectively priced collectibles or subjectively priced art — the oracle will report an educated consensus. Most importantly, Upshot makes several interesting improvements to capital efficiencies of today’s appraisal games. First, the mechanism’s valuation costs are amortized across a large number of goods, similar to price computation. Secondly, the protocol’s security margin can be assessed from future revenue: if some appraisers are malicious or bad at their job, then the protocol actively reduces their future cash flows by not selecting them for appraisal tasks. Punishing agents by cutting into their future cash flows instead of making them pay for security up front is a big capital efficiency improvement in cryptoeconomic protocols at large. Upshot’s peer prediction will be the first on-chain mechanism widely applicable to NFT price discovery, and NFT pricing will be the first application of Upshot’s protocol to roll out in 2021.

-

Derivative-Implied Pricing. NFT loans, demonstrated by companies like NFTfi, and NFT indices, as contemplated by NFTX.org, create another vector for NFT price discovery — the pricing implied by derivatives which have nonfungible assets as their underlying. Custom derivatives, such as the right to purchase an NFT in the future or prediction market shares, can potentially create NFT pricing, while delegating the costs of liquidity aggregation to other platforms or mechanisms. It’s still early in this space, and it will be developing over the coming years as the financialization trend continues.

Implications of nonfungible liquidity

Overall, the potential for capital efficient price discovery mechansims has profound implications for the liquidity of existing NFTs and, by extension, any illiquid asset which can be formulated as an on-chain nonfungible. We are likely to see a whole ecosystem of appraisal games develop around the price discovery problem in the years to come. We have also seen that some approaches are more suitable for objectively priced goods, and some more suitable for subjectively priced goods.

Here are some practical applications of price discovery.

-

A creator will be able to produce a work and an efficient market of appraisal games will offer liquidity for that work in a completely automated manner. As such, this would be an utterly disruptive mechanism for monetizing creativity, content, and digital goods.

-

Oracle-based pricing will be used to valuate portfolios and collections of nonfungibles to discover new value.

-

“Instant pricing” of NFTs can be used to create a lower bound at which holders can always liquidate their assets. Neolastics have proposed mechanisms along similar lines, and other price discovery might be applicable across a wider range of goods.

-

Any application which uses NFTs as collateral can rely on on-chain pricing to control risk. For example, a lending protocol can set liquidation margins based on automated pricing. Or, in a more technical application, optimistic rollups can potentially use this mechanism to lower “roll-off” costs for NFTs from layer 2.

-

Investors can make purchase decisions faster and more efficiently with suggested prices.

-

We can create decentralized NFT indices backed by the security of appraisal games instead of trust or collateral. This can create major efficiencies for investors seeking exposure to the NFT space but hesitant to evaluate on an asset by asset basis.

I would love to hear your thoughts and feedback on this fascinating and developing space. Follow me on Twitter @jbrukh.

References

- [Emmons] An efficient price mechanism for NFTs

- [Brukhman] Twitter thread on # NFTLiquidity

- [Ausubel, Milgrom] The lovely but lonely Vickrey auction

- [Brukhman] All digital content is going on-chain

- [Berenzon] Constant function market makers: a zero to one innovation

- [Hubert] Niftex: The buyout clause in depth

- [Emmons] Peer prediction 101

Disclaimer: The content provided on this site is for informational and discussion purposes only and should not be relied upon in connection with a particular investment decision or be construed as an offer, recommendation or solicitation regarding any investment. The author is not endorsing any company, project, or token discussed in this article. All information is presented here “as is,” without warranty of any kind, whether express or implied, and any forward-looking statements may turn out to be wrong. CoinFund Management LLC and its affiliates may have long or short positions in the tokens or projects discussed in this article.